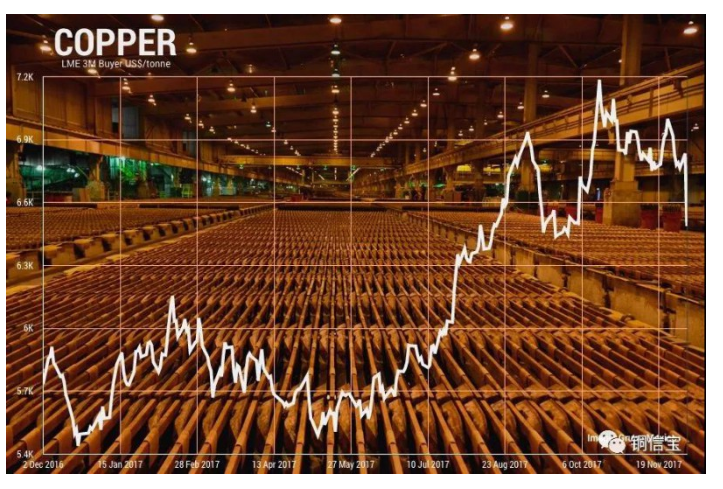

Depth|The top of the copper price may have appeared!

For the macro signal of copper, Huachuang Securities believes that it should pay attention to two aspects, economic aspects, and China and the United States industrial production. In terms of finance, look at the year-on-year China-Europe broad currency.

There are two questions that need to be answered at the moment. First, from a financial point of view, what are the signals suggesting? China and Europe's broad currency will likely fall back in the second half of the year, and copper prices will have downward pressure. In terms of broad currencies in Central Europe:

1) One party needs to pay attention to the growth rate of broad money in China and the Eurozone itself. Taking into account the slowing down of social financial growth, there is a high probability that in the second half of the year, it will first decline and then rebound slightly. China's M2 growth rate may be flat in the second half of the year. In the Eurozone, even assuming that the amount of new M3 growth in the second half of the year is the same as the same period last year, the growth rate of M3 by the end of the year is basically similar to the current 8.3%.

2) On the other hand, we need to pay attention to the influence of exchange rate factors. In fact, taking May of this year as an example, the year-on-year growth rate of broad money in China and Europe was 19.6%, of which 11.5% was driven by exchange rate factors. This means that assuming that the current exchange rates of the RMB and the Euro remain unchanged, starting from the second half of the year, subject to the high base of the exchange rate of the same period last year (the RMB and the Euro appreciated sharply in the second half of last year), the pull of the exchange rate will fall back to around 0%.

Taking the above two factors into consideration, we estimate that the broad currencies in China and Europe will have greater downward pressure in the second half of the year.

Second, from an economic perspective, what are the signals suggesting? Industrial production in China and the United States was flat compared to the second half of the year, and copper prices tended to fluctuate. China's industrial production has fallen slightly in the second quarter, and may continue to fall as exports fell slightly in the second half of the year. For the United States, the inventory data we continue to pay attention to show that the United States may have entered a stage of passive inventory replenishment, and the upward trend of industrial production will further slow down. Overall, industrial production in China and the United States showed a flat trend in the second half of the year.

The combination of the two angles means that the top of the copper price may have appeared, and it may be difficult to exceed the previous high in the second half of the year.

If copper prices reach new highs, what kind of catalysis is needed?

Compared with the copper price trend after the 2008 financial crisis, there was a relatively large correction in mid-2010, and then it hit a new high again.

From a macro perspective, it is not difficult to know the reason for the second rush. On the one hand, China and the United States have actually moved up unilaterally in 2010 after the adjustment of the base of industrial production. (Figure 1, yellow line). On the other hand, the United States conducted the second round of QE in the second half of 2010, exceeding expectations. This led to the second bottom of the U.S. dollar index in the second half of 2010, and the central and European broad currencies hit a second high year-on-year.

Will there be another record high now? Unless it is catalyzed by the following factors. One is that the economy has exceeded expectations. Industrial production in China and the United States continued to rise in the second half of the year. Or monetary policy exceeds expectations. For example, the US monetary easing has exceeded expectations. For now, the probability is low. However, given that the impact of the epidemic is complex and changeable, we need to stay concerned.

News source: Cable Network

Weicax

Weicax